Market Updates and Commentary

Equities moved higher yet again last week — following a very brief and shallow decline the prior week. The S&P 500 Index gained 1.54%1, notably small-capitalization stocks were up 5.06%2. A hefty portion of the small-cap gain followed Jay Powell’s speech on Friday. Small caps have struggled over the last few months along with cyclicals. The 10-year Treasury yield moved up to 1.31% through Friday. Yields and bond prices move opposite each other. In addition to presenting a difficult bond dynamic, the 10-year yield is indicative of economic sentiment. An increasing yield and steeper curve are associated with stronger growth and inflation. Underlying stock-sector performance has been heavily influenced by the 10-year yield this year. If the 10-year yield continues to push through 1.4%, this would support equity performance rotating back in favor of small caps and cyclicals.

A rotation of this sort would be a healthy development — giving the market a shot at consolidating or grinding higher as opposed to further stretching the narrow leadership of the last few months. Equities still have a positive liquidity backdrop, which continues to fuel the buy-the-dip market of 2021. The speed and shallowness of pullbacks has been surprising. Our canary in the coal mine of credit stress is not present. Additionally, consumer credit is quite positive. The historic S&P six-month return data relative to the current Conference Board U.S. Leading Credit Index is bullish.

Source: Renaissance Macro Research, Haver Analytics

Economic News

The rising 10-year yield last week is also sending a message that the peak to the current COVID surge is moving into sight, as the surge is the primary economic growth concern. COVID cases and hospitalizations are continuing to rise but at a slower pace. Initially, hard-hit southern states appear to be peaking. The economic impact of the surge appears to be very localized, slowing some economic momentum, but not reversing it.

Source: Renaissance Macro Research, Macrobond

The economic news of last week centered around the Federal Reserve Jackson Hole symposium on Thursday and Friday. Much attention was paid to Fed Chair Jay Powell’s speech on Friday morning which successfully threaded the needle the markets were hoping for. While indicating that the Fed would begin tapering the monthly bond purchase program before the end of this year, Chair Powell also pushed back against the notion that the Fed would begin hiking short-term rates anytime soon. The summary conclusion: the Fed is going to let growth and inflation run hotter for the time being.

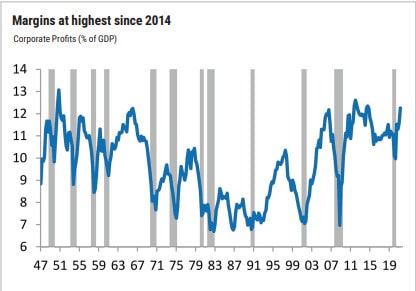

Additionally last week, Q2 GDP was revised slightly higher. Notable in this release were corporate profits, which are at their highest level since 2014 relative to nominal GDP. This bodes well for corporate investment in coming years.

1 MarketWatch

2 Russell 2000

Past performance is no guarantee of future results.

Cary Street Partners is the trade name used by Cary Street Partners LLC, Member FINRA/SIPC; Cary Street Partners Investment Advisory LLC and Cary Street Partners Asset Management LLC, registered investment advisers.

This information was prepared by or obtained from sources believed to be reliable, but Cary Street Partners does not guarantee its accuracy or completeness. Any opinions expressed or implied herein are subject to change without notice. The material has been prepared or is distributed solely for information purposes and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. An investor cannot invest directly in an index.

CSP2021171 © COPYRIGHT 2021 CARY STREET PARTNERS LLC, ALL RIGHTS RESERVED.